A Simple Overview: Junior ISAs in Times of Rising Interest Rates

As the financial climate shifts, especially with the rise in UK interest rates, many might find short-term deposit rates more attractive. These rates often present themselves with a sense of stability and an appealing return. But before making any financial decisions, especially concerning investments like a Junior ISA, it’s essential to be informed about the broader financial picture, so we’ve taken a look at how investments perform against cash over the long term based on some historical data.

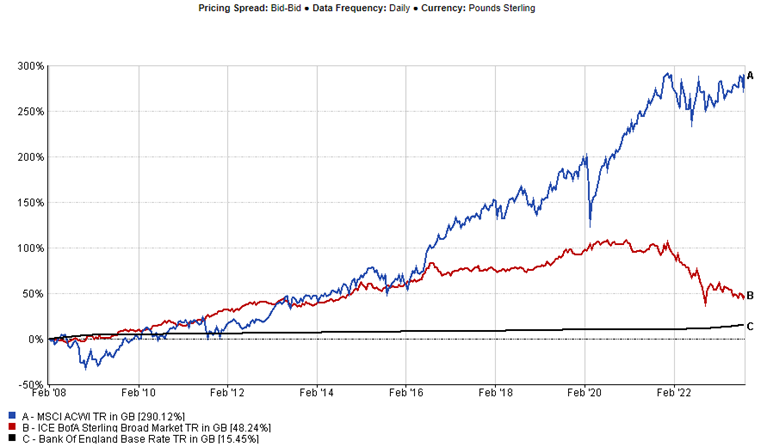

Historical Trends of Equities, Bonds, and Cash

The data indicates that there have been periods where cash rates were very competitive. However, over more extended periods, equities and bonds have shown much greater patterns of return. For example, records from February 2008 to August 2023 highlight varying performance levels of these assets. The chart below shows the performance of Sterling Bonds (in Red), Global Equities (in Blue) and cash invested at the UK Base rate in black from February 2008, the last time rates were this high – 15 years ago.

Stretching to an even longer-term perspective, a study from Sarasin & Partners, looking back since 1900, presented the following average annual returns:

- US Equity: 10%

- UK Equity: 9.1%

- Gilts: 5.3%

- Cash: 4.5%

- Inflation: 3.7%

Source: Sarasin & Partners Compendium of Investment 2022

Inflation Rates Over Time

The UK’s inflation rate has historically fluctuated. Records show it has averaged just over 2% since 1990. However, as of July 2023, this rate stands at 6.8%. When considering investment vs. cash it’s vital to understand how inflation rates have varied over time and their potential impact on the real value of money. Again, Sarasin & Partners have calculated the effect of inflation on cash over time below:

| Inflation Rate | How long it would take to halve your money? |

| 2% | 30 years |

| 5% | 14 years |

| 9% | 8 years |

| 10% | 7 years |

Source: Sarasin & Partners, August 2023

The Framework of Personal Saving Allowance (PSA)

The PSA structure means that there are thresholds up to which interest earned on savings remains tax-free. Here’s a breakdown:

- Basic 20% rate taxpayers: Up to £1,000/year interest tax-free.

- Higher (40%) rate taxpayers: £500/year tax-free.

- Top (45%) rate taxpayers: No PSA.

With rising interest rates, basic rate taxpayers can exceed their £1,000/year tax-free interest allowance with just £20,000 saved, while higher rate taxpayers can with around £10,000 saved and top rate taxpayers don’t benefit from a PSA. Taken together the confluence of inflation and high interest rates makes cash seem much less attractive when stacked up against long-term investments.

The financial world is vast and multifaceted. When considering any investment, it’s crucial to be informed and to understand historical data and the present context. Knee-jerk reactions to headlines are rarely a good idea in a financial context. Like all investments, a Junior ISA can go up as well as down, and there’s a potential risk of ending up with less than what you initially invested. If you want to see how our Junior ISA could perform based on historical performance and with regular contributions check out our calculator here.